Regulated or Unregulated Finance – Which would you choose?

Unregulated Finance Agreements and Regulated Agreements – Yet more comment, back by popular demand

Fighting the establishment to protect ordinary Folks

Sharp practice usually means someone gets cut!

What is the difference between an Unregulated Finance Agreement and a Regulated finance agreement?

Once again, I am writing to highlight the importance between a Regulated and Unregulated Finance Agreement – and your consumer rights with both.

We recently helped a customer who had just signed an agreement with another lender but wasn’t comfortable with the agreement he had been asked to sign, and wanted clarification before the drawdown date. Upon closely inspecting the paperwork for his finance agreement, our customer noticed the documentation for the funding of his car expressly stated that his classic (a 1980’s classic Porsche was to be used ‘wholly or predominantly for the purpose of business’ Not what he asked for and not the case.

This is where our story begins.

So, you want to buy a car (or refinance something you already own). Simple right?

You apply to a lender and they carry out the necessary checks.

They value the car and offer you a loan facility secured against it.

You agree to a period of (say) 48 months, maybe with a balloon payment to offset the monthly payment.

Off you go looking forward to paying off that loan and owning the car as soon as you can…. Simple right?

You may choose to work with an intermediary (Broker) or be tempted to go directly to a lender.

The C Word

We all know this loan facility as good old- fashioned Hire Purchase but through this application process did anyone mention the word CONTRACT? Suddenly the whole atmosphere of the loan becomes legally serious, it’s a strong word and we all know it or certainly should do. After all, in the loan market all the people that operate in it are:

– licensed under legislation created by the Financial Conduct Authority…

– and have a duty of care…

– and are legally obliged to ensure that your wants and needs are fully qualified…

– and those needs are subsequently serviced with correct and balanced advice…

– whether it directly benefits them or not…

aren’t they?

There are two levels of Hire Purchase agreement:

A Regulated Finance Agreement and an Unregulated Finance Agreement

We need to define the difference between the two and why they exist as separate entities.

Both hold the asset they are loaning against as security and typically hold the same option of length of term.

What is the difference between a Regulated and an Unregulated finance agreement?

Regulated Hire Purchase or a Rnregulated Finance Agreement:

Regulated Hire Purchase or a Regulated Finance Agreement is often referred to as Consumer Finance, eluding to the fact that:

Joe Bloggs (the average man on the street) borrows money to buy an item and may need protection from the law during and after that process.

What does this mean?

It is assumed that you may not necessarily have business acumen and fully understand the terms of the contract and what you are entering in to and strictly becomes the responsibility of the lender to fully educate you into your responsibilities and rights under their agreement.

The document has total consumer flexibility as a result, allowing capital over payments and uses the FCA formula of no penalties if you decide to settle off the loan prior to the agreed period, and carries the ever-important VT (Voluntary Termination Clause).

A lender or intermediary who offers a Regulated Hire Purchase agreement must be fully licensed and qualified to do so. He has a duty of care to ensure that you can afford the payments and fully understand the contract you are signing. Clarity and professional advice are the key and closely monitored by the regulator on a regular basis.

Unregulated Hire Purchase or an Unregulated Finance Agreement:

This is often referred to as HNW (High Net Worth) or Business Finance.

a business principle or a HNW Individual seeks to borrow money on an asset he is assumed to be more experienced in life and or business so does not require the same level of protection.

What does this mean?

Joe Bloggs the Company Director / Chair Of The board / Limited Company Itself (ie. not the average man on the street) borrows money to buy an item for himself or for his business and is assumed to be more experienced in life and/or business so does not require the same level of protection as Joe Bloggs (the average man on the street)

The assumption is that when a business principle or a HNW Individual seeks to borrow money on an asset he is assumed to be more experienced in life and or business so does not require the same level of protection. He should understand what he is signing right?

So, in this case, the lender can apply their own early settlement formulas and the lender has far greater rights in a court of law to recover their asset quickly if the hirers fall into arrears for whatever reason.

An unregulated agreement offers less flexibility in terms of over payment and has less obligation to accurately explain the contract to the hirer.Overall it is a much looser, less regulated environment with more benefits towards the lender.

Why are we seeing a rise in unregulated agreements in classic car finance?

Until recently a regulated facility was only available up to a loan level of £62,500 automatically making a loan above this level qualifying to be unregulated.

I say until recently as many lenders now offer regulated loans into the millions for the right candidate on the basis of ensuring their service offering is diverse and fair. If they are licensed to offer a Regulated Facility (not all are), then it’s a major benefit for the buyers in the market.

On this basis why would any individual (Ltd Companies aside) want an unregulated agreement?

Now here is the snag – say a lender or intermediary isn’t licensed to sell Regulated Consumer Finance or is reluctant to offer it because of the professional restrictions it imposes on them and their operation?

Companies can obtain licenses to sell money, but the license to sell regulated money is extremely strict. So how does a lender persuade you to sign an unregulated finance agreement when you could be signing a regulated agreement with the full benefit and protection of the law on your side?

Sounds quite blunt doesn’t it?

In the current climate of protective regulation this is almost unbelievable, however, it is out there and it’s out there in a very big way.

To recap, a Regulated Hire Purchase agreement must be explained fully to the consumer by a licensed professional, your rights and exposure under the terms of the agreements must all have been made clear and in a court of law the lender has a drawn-out process of recovering the car if you fall into arrears.

An Unregulated facility is where you waiver those rights and become more exposed to the terms and conditions of that lender and by definition have little recourse if you are miss-sold in any way at all.

An increase in loans and finance agreements with less rights for the customer? How are they getting away with it?

If a lender wishes to sell (I use the term literally) agreements to the value of £62,500 and below but only have an Unregulated facility, how do they do it?

Book Building – How long will your finance provider really be around?

In recent years the classic and supercar finance sector has seen an emergence of capital companies, whose sole purpose is to sell large lumps of money into the market – book building, if you will. These companies may talk the talk, but their sole aim is selling the book for the major benefit of shareholders. With this there has been a decline in the quality of advice, with the consumer paying the price. If you are borrowing more than the benchmark £62,500 then assuming you meet the HNW status you could be steered towards an unregulated loan, and why would you waive your consumer rights when there are so many alternative lenders offering protected loans?

How does the rise of unregulated finance agreements affect classic car enthusiasts?

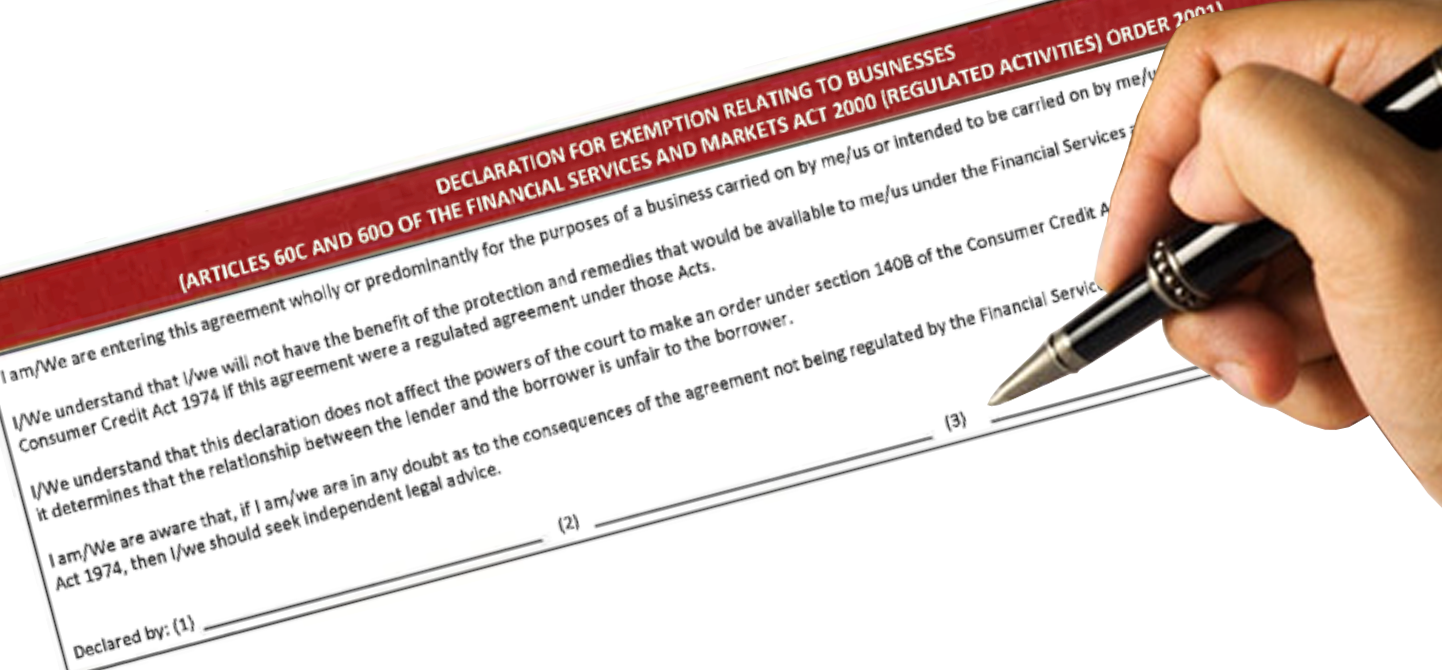

An Unregulated finance document usually has a Business Mileage Exemption box buried amongst the text.

This is where you can be asked to sign and legally declare that the car will be used for business mileage, waiving your ever-important Consumer Rights and enabling the lender to apply unregulated terms.

Scenario – How it works in practise

You want to buy a £49,000 classic Porsche for weekend use, shows, club events and the odd holiday.

You go to market and request a quotation for a loan.

You agree to the numbers with a lender and someone appears on your doorstep with a finance agreement.

You sit in the comfort of your own home and are asked to sign the documents as the car is to be collected within a few days.

Everything seems easy and quite straight forward, quite efficient in many respects. You start to look through your copy of the agreement (if you were left one) and see that the heading on the papers indicated Unregulated Hire Purchase but are not quite sure what this means as it wasn’t explained clearly.

On reading through the document, you see that one of the boxes you were asked to sign has a heading of Declaration for Exemption relating to Business which you are not but you signed it because you were asked to.

By signing this you have voluntarily excluded yourself from FCA protection and entered into an Unregulated Agreement.

This naturally raises questions as to what you have signed.

You have technically made a false declaration and signed to that effect.

You only insure the car for limited mileage each year and let’s face it, would you buy such a car for business use when it is clearly a collectable?

If alarm bells are ringing then indeed they should be.

You have made a false declaration and played smartly into the hands of the finance company with an agreement that gives you very little protection as a consumer.

Ah, the word Consumer!

Yes, as the car is only £49,000 you should have been treated and advised as to the correct facility and a Consumer Regulated Hire Purchase agreement is what you should have been advised.

You think, ‘this is OK, I can complain and put things right’ but your signature on the document says otherwise.

“But he didn’t explain it to me, surely the lender has an obligation to check that I understand the documents?“, we hear you say…

Well no, not with an unregulated agreement.

The lender has a duty of care but this is not an obligation – he/she doesn’t have to.

So, let’s sit in front of the Judge for a moment –

Judge to client –

Judge – “Did you sign the Un regulated document that was presented to you”

Client – “Yes your honour!”

Judge – “Was the detail of the document and your rights or exclusions under the terms of the document explained to you?”

Client – “Not clearly your Honour”

Judge – “Did you make a false declaration on that document about the car being for business use and have that car insured only for limited mileage use as a classic car?”

Client – “Un knowingly – Yes, your Honour!”

Judge – “Do you feel that you were misled and not professionally informed about what you were being asked to sign?”

Client – “Yes, your honour!

Judge – “Are you aware that you may have broken the law by signing a declaration that clearly isn’t true?”

Client – “No, your honour”

Judge to lender –

Judge – “Did you explain the document in detail to your client?”

Lender – “I felt I had your honour”

Judge – “Did you explain that he was making a potentially false declaration by signing the box you asked him to?

Lender -“No, your honour”

Judge – “Can you explain why you didn’t go through the fine detail in the agreement so that he understood it and explain why he was signing each and every part you asked him?”

Lender – “It’s an unregulated document your Honour, I don’t have to!!

Judge – “Would you say that you have sold an Un Regulated agreement to what should be a Consumer Regulated Customer and denied him full protection of the law for the benefit of your company when all he wanted was to buy a weekend classic car on a simple loan?”

Lender – “I have a target to meet your honour!”

Summing up –

In conclusion, this practice is sharp, unprofessional, unfair and misleading but is it illegal?

We need to ask the Financial Conduct Authority about that.

Classic & Sports Finance have been around for a long time and some of our customers have been with us for more than 20 years (and that makes me feel old!) but intend to be around for a good few years more, our commitment to customers, doing the right thing, and delivery quality will not change.

{kind=link}