The state of the classic car market – April 2015

There isn’t a definitive mechanism for ascertaining the health of the classic car market. Most of the available “indexes” concentrate on specific areas of the market; the well known HAGI Index focuses on a very specific and relatively small list of collectors cars and the newer K500 index looks at a broader, hand-picked range of collector and popular classics. We like the Hagerty Market Rating Index, which looks at the market as a whole and combines what is almost certainly the largest global database of classic car values to give an easy to understand reading – the only problem is, it currently only measure the US market…

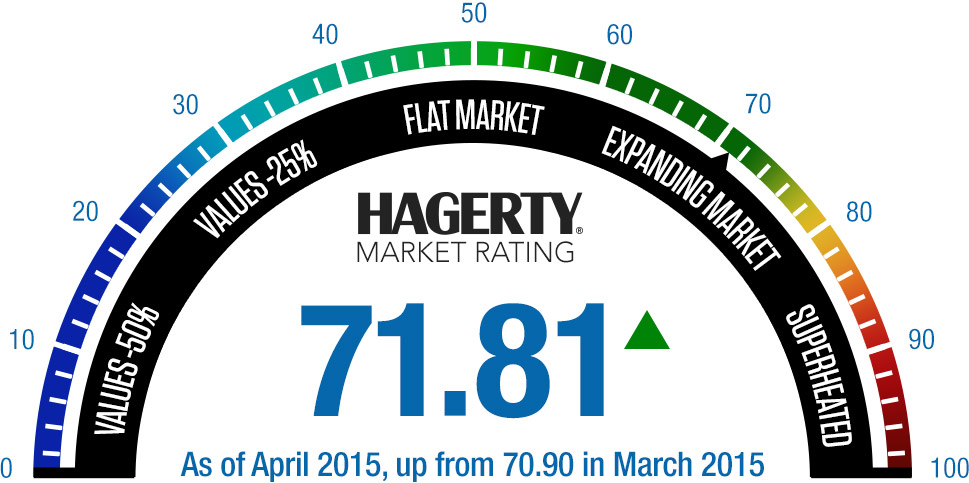

The Classic Car Market – April 2015

Hagerty’s US market rating increased this month for the following reasons:

- Expert sentiment is up in the wake of strong middle-market sales at Amelia and extremely rational bidding at the very top of the market. Year-over-year dollar volume was up over 30% at Amelia, but part of that can of course be attributed to Bonhams’ entry into the Amelia Island auctions for the first time in 2015.

- Private sales were extremely robust in March. Average sale price was up 13% year-over-year.

- The percentage of cars selling at about their insured value was at an all-time high. Over 36% of private sales tracked were at amounts in excess of insured value

Strong middle market sales are reflected in the UK market and we would translate “rational bidding at the very top of the market” into “no-one went mad, sensible prices were paid”.

Hagerty Market Rating – historic view

The HAGI Index reported falls in their TOP 50 Index of around 1.6% which takes the index back to a value last seen in October/ November 2014. Their Ferrari (HAGI F) and Porsche (HAGI P) indices both saw small drops compared to February of 1.7 and 3.3% respectively while surprisingly the HAGI MBCI (Mercedes-Benz) index went up by 1% – we haven’t noticed a rally in Mercedes prices. Year to date their indices generally show minute corrections of fractions of a percent with the exception of Ferrari which is up around 1% YTD. HAGI cited currency as one of the main influencing factors and the strengthening dollar will also have had a positive effect on Hagerty’s US rating. The middle market cars of the eighties had a positive influence.

The K500 index stands at 444.5 from an opening position on 1 December 2014 of 449.9, and this reveals a static market in their eyes with some (possibly short-term) winners in more recent Ferraris and a slight decline in what have been seen as ‘blue chip’ cars such as the Mercedes-Benz 300 SL.

The Classic & Sports Index

Strictly speaking we don’t have an index but we do see a very high volume of deals and transaction every month. Auction results have been less exciting and impressive than last year (we’d probably describe them as “in decline” at this point in time) but dealer activity is still very strong with buyers willing and able to spend significant sums on the right cars and if anything this appetite is increasing. Given that auction activity only represents 5-10% of classic car transactions, the market is still buoyant and healthy – probably the biggest threat to its stability are unscrupulous sellers and speculators who are arriving in the market place in increasing numbers. So, to sum up;

Outlook – currently stable. Appetite – strong.

Many thanks are due to Hagerty UK for their support and cooperation in allowing us to share their data. We hope to extend this direct sharing of information to the other indices in the very near future.

{kind=link}